2014 Performance of Construction/Real Estate Equities

Dolapo Omidire . 9 years ago

equity markets

investment

julius berger

nigeria reit

nigerian real estate research

nigerian stock exchange

oil prices

premium

real estate

real estate research

reit

research

Share this post

Subscribe to our newsletter

In 2014, downward spiraling oil prices, volatile currency markets and insurgency overshadowed Nigeria being named Africa's largest economy. As foreign investors exited and bears dominated the investment landscape, the performance of core asset classes was abysmal. Equity markets were initially on course to produce ±-20% at year end, however a slight rebound in the last weeks of December allowed…

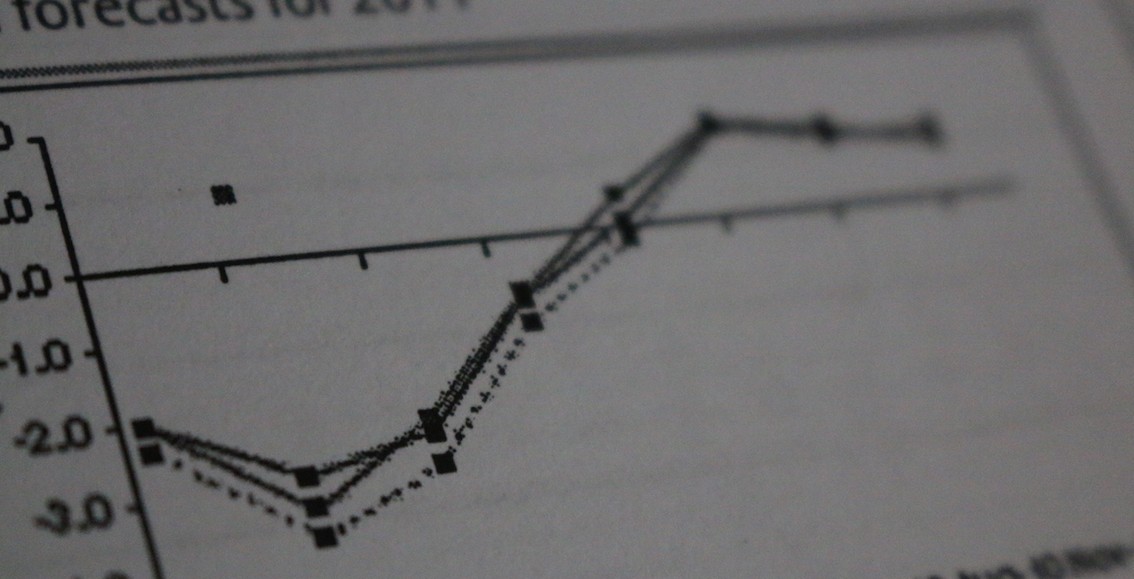

In 2014, downward spiraling oil prices, volatile currency markets and insurgency overshadowed Nigeria being named Africa’s largest economy. As foreign investors exited and bears dominated the investment landscape, the performance of core asset classes was abysmal. Equity markets were initially on course to produce ±-20% at year end, however a slight rebound in the last weeks of December allowed for a marginal recovery, meaning that the Nigerian All Share Index was able to return -16% for 2014. The performance of the Construction/Real Estate sector was better but not impressive at -6.51%.

Left – 2014 Nigerian All Share Index. Source: Bloomberg. Right – 2014 Brent Crude. Source: Nasdaq

The table below shows that the performance from most equities in the sector was negative, with only Arbico, Skye Shelter Fund and UPDC REIT providing meagre positive returns of 4.95%, 5.25% and 5.6% respectively. Rising revenues arguably supported interest in Skye Shelter Fund during the course of the year. Other equities like Costain, UAC Property Development Company and Roads Nigeria performed disastrously returning -40.32%, -35.9% and -25.65% for 2014 investors, conceivably caused by the aggressive sell down pressure from bearish investors across board.

Source: estateintel.com. Data Adapted from Bloomberg and Nigerian Stock Exchange

Currently only 10 Construction/Real Estate sector companies are listed on the main board. Of this 10, 4 firms including Julius Berger, UPDC REIT, UAC Property Development Company and Union Homes REIT account for 96% of the sector’s market cap. Julius Berger alone accounted for 57% at year end 2014, with a market cap of over N80bn.

Though Julius Berger fell -4.3% in 2014, it still holds promise for mid-long term investors. The firm was named the construction partner for the ambitious Centenary City development in Abuja, which will include 260 Luxury Villas, 265 Apartment Buildings, 139 Office Buildings, 308m high mixed use Africa Square and Tower, 5 Major Retail Centers and much more. They will also be working with General Electric (GE) as they have emerged as the preferred bidder for their multi modal manufacturing and Assembly facility in Calabar, Nigeria. These 2 factors, coupled with their prior and imminent success with projects like Lekki Ikoyi Link bridge, Rose of Sharon Tower, Nestoil Tower and others on the Eko Atlantic should mean that they have good prospects for revenue growth in the future.

To some extent, it is disappointing that the Construction/Real estate segment of the Nigerian Stock Exchange is largely dominated by construction companies. Of the 10 listed, UPDC is the only property developer, while the other 3 are run-of-the-mill REITs, demonstrating that the depth and breadth of the Nigerian listed real estate sector is still very rudimentary. On the New York Stock Exchange, hundreds of REITs, real estate service providers and real estate investment funds/firms are listed.

Even so, the Construction/Real Estate segment of the Nigerian equity market only accounts for 1.22% of the capitalisation of the entire market. N139bn of N11tr at of end of 2014. On the Johannesburg Stock Exchange, REITS account for approximately 2.3% of the entire market, this discounts construction companies, property companies and real estate service providers. Nonetheless, Haldane McCall REIT intends to complete its IPO by January 14th, to be listed later this year. With a relatively small capitalisation of N13.39bn, it should aid the growth of this sector moving forward.

Looking into 2015, elections, oil prices and insurgency are just a handful of the problems that Nigeria will be facing, an indication that capital markets in 2015 may not be pleasant, especially in the H1. Some investors are looking to the agriculture sector to drive growth, while others are leaving equities all together and ploughing their capital into fixed income and direct real estate. However, the problems noted should only drive the markets in the short term; mid-long term investors will be keen on liquidity, transparency, and the level of growth in Nigerian capital markets.

Related News

You will find these interesting

Bisi Adedun . 5 months ago

Africa Investment Forum

AIF

Bisi Adedun . 5 months ago

housing

personal finance

Bisi Adedun . 5 months ago

Century city

New City